Companies that engage in lending activities often estimate potential losses they might experience due to credit risk therein involved. So they make provision estimates in relation to the loans that are likely to become delinquent or bad. In line with the Accounting principles the institutions have to provide for the these expected losses which are treated as expenses on the company's financial statements.

In Loan Performer the provision figure is arrived at by setting and calculating the provision periodically. You can also optionally update your accounts with the calculated provision amount, but to do this you need to set the provision accounts at System/Configuration/Loan Product Settings/GL Accounts 1/2.

Note: 1. A Loan provisioning is an expense that is reserved for default/bad performing loans/credits.

2. It is an amount that is set aside as an allowance for bad loans or credits.

3. These loans may be delinquent (Late) on their repayments or default the entire loan. This can create a loss to the institution on expected income.

Also note that Loan Performer Computes loans based on three categories of loans

i Normal (Healthy Loans)

ii Rescheduled loans and

iii Refinanced loans

The bookings that will be made after loan provisioning, loan write-off and Repayment of Written-off Loans Report will be as follows:

At loan provisioning

Provision costs for bad loans account

Debit

Provision for bad loans

Credit

At loan write-off

Provision for bad loans

Debit

Loans written of accounts

Credit

At repayment of written off loans

Cash/bank

Debit

Recovery of loans written off accounts

Credit

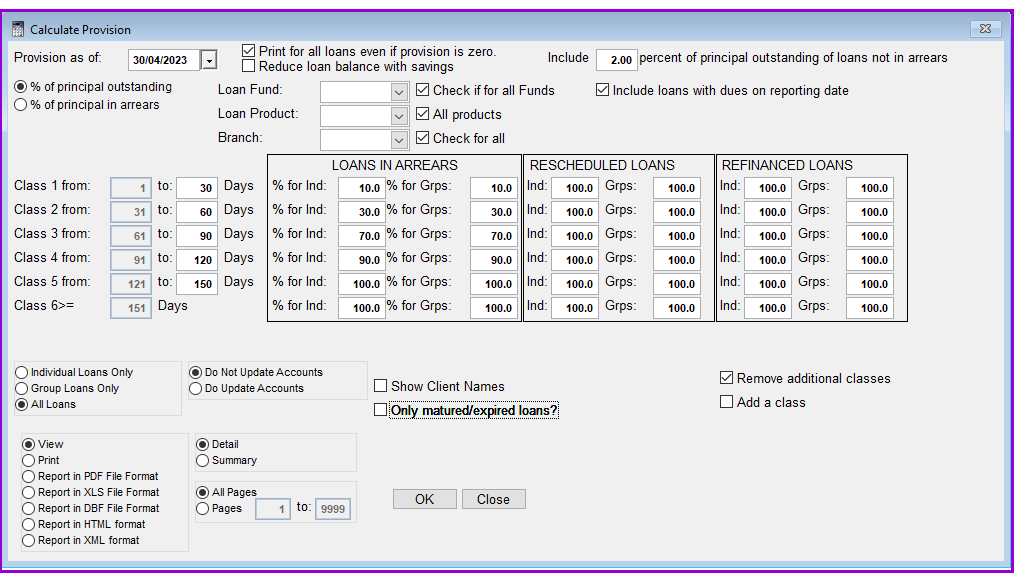

How to calculate provision

To calculate loan provision you go to Account/Calculate Provision and a screen will be displayed as follows:

Provision as of: Enter the date as of when the provision should be calculated, e.g., "30/04/2023" The default date is the last date of the month before the current login date.

Print for all loans even if provision is zero: If this option is ticked then the provision report will display all the loans at the time of loan provisioning. This means that loans that are not delinquent will also be displayed.

Reduce loan balance with savings: If you tick this option, then the outstanding balance for each loan will first be reduced by the available savings balances before being considered for provisioning. The remaining balance will then be used in the loan provisioning process.

Example: If a delinquent loan has as outstanding balance of Ugx 1,000,000 and the client still has savings of Ugx 300,000 then the amount to be used during the provisioning will be only (1,000,000 - 300,000) = 700,000.

As % of principal outstanding: If you select this radio option then the amount to be used in loan provisioning will be the total outstanding principal for all delinquent loans.

Example: If a loan of Ugx 1,000,000 has only one installment of UGX 100,000 in arrears then the whole outstanding of Ugx 1,000,000 will be used during the provisioning.

As % of principal in arrears: Under this option the only the part of the principal that is in arrears will be used for provisioning.

Example: If a loan of Ugx 1,000,000 has only one installment of Ugx 100,000 in arrears, then only the Ugx 100,000 that is in arrears will be used during the provisioning.

Loan Fund: Loan Performer can calculate provisions for specific or all funds. From the drop down list select the fund that you want to calculate the provisions for. You can also tick the Check for if for all funds checkbox to calculate the provision for all funds.

Loan Product: Loan Performer can calculate provisions for specific or all products. From the drop down list select the product that you want to calculate the provisions for. You can also tick the For all products checkbox to calculate the provision for all funds.

Branch: From the drop down select the branch that you want generate the Loan Provision report. This is possible when you have a multi branch database.

Include ..... percent of principal outstanding of loans not in arrears: If you want to make provisions for non delinquent loans then enter, in this text box, the percentage by which the non delinquent loans will be provided for, e.g., "2%".

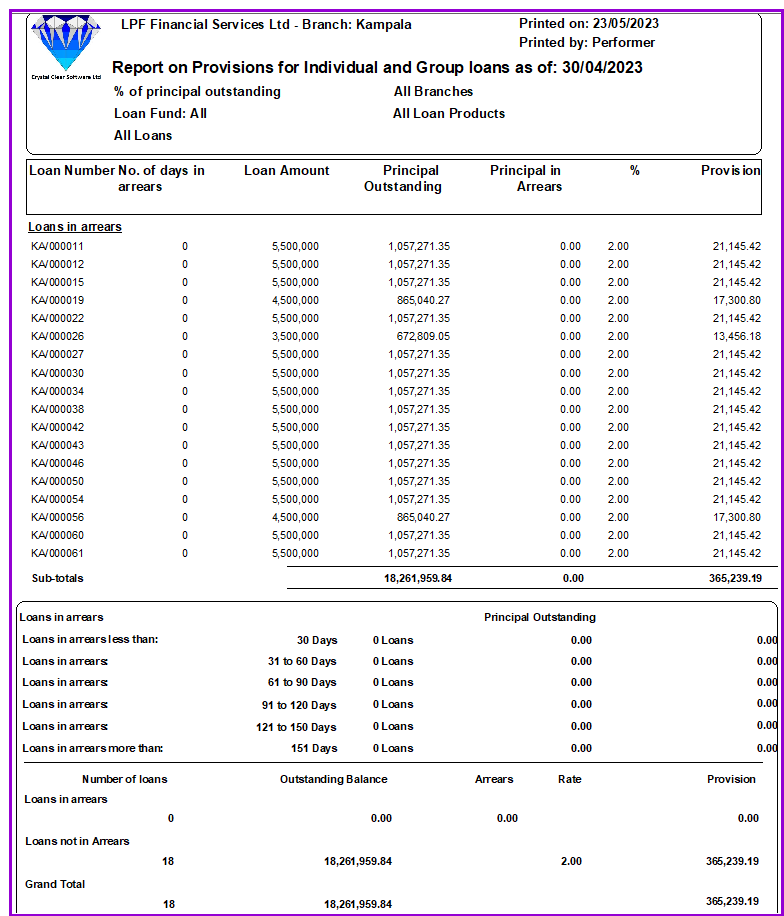

Note that in the absence of loans in arrears, the system will only calculate and provide the percentage of the out standing balance of principle i.e. if it was indicated in the field "Include percent of principal outstanding of loans not in arrears". In the above case it was 2%

Note that provisioning is done for different Classes that are set according to the number of days that the loans are in arrears. Different percentages are set for each age class according to the default probability of that class.

Class 1 from ................. to ................ Days % for Ind: ................ % for Grps: ................: For each class range enter the number of days to be used and then enter the percentage that should be used for the individual and group loans that fall in this class range, e.g., from "1" to "30" days with "10 %" for Individual Loans and "10 %" for Group Loans. You can then continue to define the class ranges and percentages for Classes 2, 3, and 4.

Add a class: If you need to add more classes to the default 5 then click on the Add a Class button and an additional class will be displayed with an option to add the 7th one where you will be able to define the new range and percentage as seen below:

Do not Update accounts: After the provision has been calculated, you have the option of either Updating the accounts with the calculated provision or not. If you select the Do not Update Accounts radio button, then the calculated provision will be displayed but the accounts will not be updated.

Do Update Accounts: If you select this option then the accounts will be updated with the calculated provision after you view and print the report.

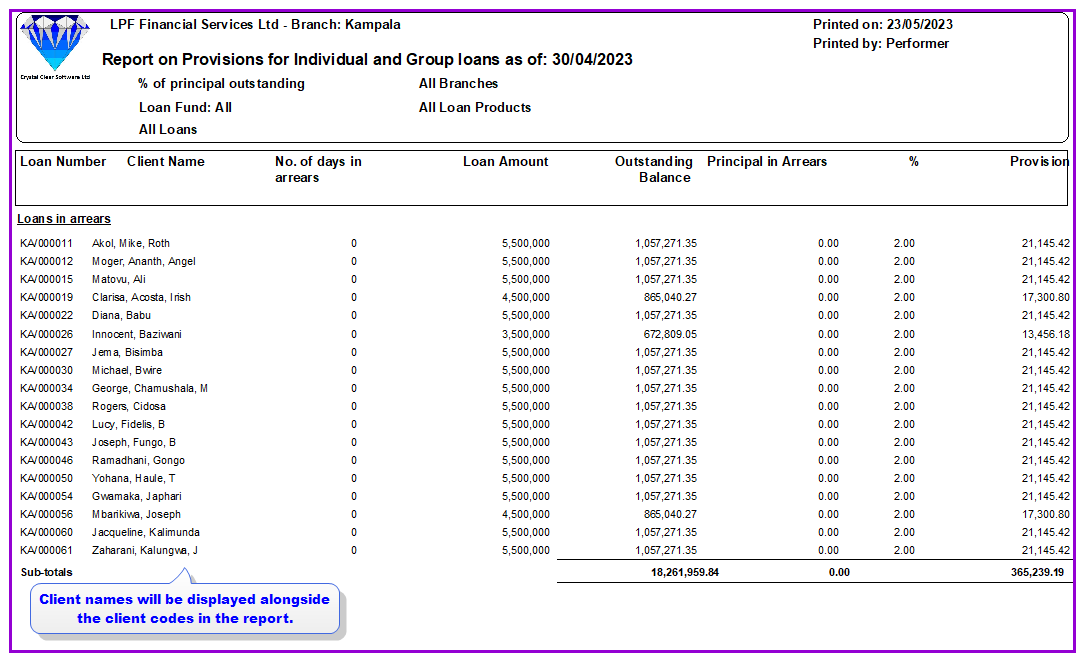

Show Client Names: When this option is selected then the client names will as well be displayed in the provision report along side the loan numbers as seen below.

Show Client Names: When this option is not selected then the client names will not be displayed in the provision report as seen below

Note that by default client names are not displayed in the provisioning report.

Only matured/expired loans: Select this option if you want to calculate provision for only the Matured or Expired Loans. This means that the calculated provision will exclude all active loans.

Note that Loan Performer allows you to calculate provision for Individuals only, Groups only or Both.. Choose the option you want to use from the radio options given.

Select any other required additional options or use the default selections. For additional information on these options you can refer to Accounting Report Formats.

Click on the OK button to calculate the provision. The following Provision report will be displayed showing the details as they were set up during the provision calculation:

Note that if you set the Option "Do not Update Accounts", then Loan Performer only prompts you to save the Provision Calculation parameters set above. Click on the Yes button to save the parameters for futures reference. However if you set the option "Do Update Accounts" then Loan Performer will prompt you to print the displayed report before updating the Account. This means that if you don't print the report then the accounts will not be updated with the calculated provision..

The loan provision amount calculated will be booked on the loan loss reserve account defined at System/Configuration/Loan Product Settings/GL Accounts 1/2. When writing off loans at menu Loans/Write off loans, the user won’t be able to proceed with the operation if the amount of loan provision is less than the total amount of loans to be written off. The user will receive a message that the “Loan Loss reserve is depleted” and will be required to increase the provision for bad loans first.